The Finance Act 2025 has introduced a major change in the tax treatment of profit on bank deposits and other debt instruments. This amendment directly affects salaried individuals, retirees, business owners, investors, and anyone earning profit from savings accounts or fixed deposits. Many people are surprised to see lower net profit credited by banks, and this change explains why.

In this article, I will explain what has changed, who is affected, who is exempt, and how much extra tax you will now pay, all in simple words.

What Is “Profit on Debt”?

Profit on debt means the income you earn from money deposited or invested, such as:

- Bank savings accounts

- Fixed deposits

- Term deposits

- Investments in government securities

- Financial institution deposits

This profit is taxed at source, meaning the bank deducts tax before crediting the profit to your account.

What was the tax rate before the Finance Act 2025?

Before this amendment:

- Tax on bank profit was 15%

- Non-filers paid 35% tax on profit on debt

- National Saving Schemes had separate tax rates

This system remained in place for several years.

Learn more: Income Tax Return Master Course

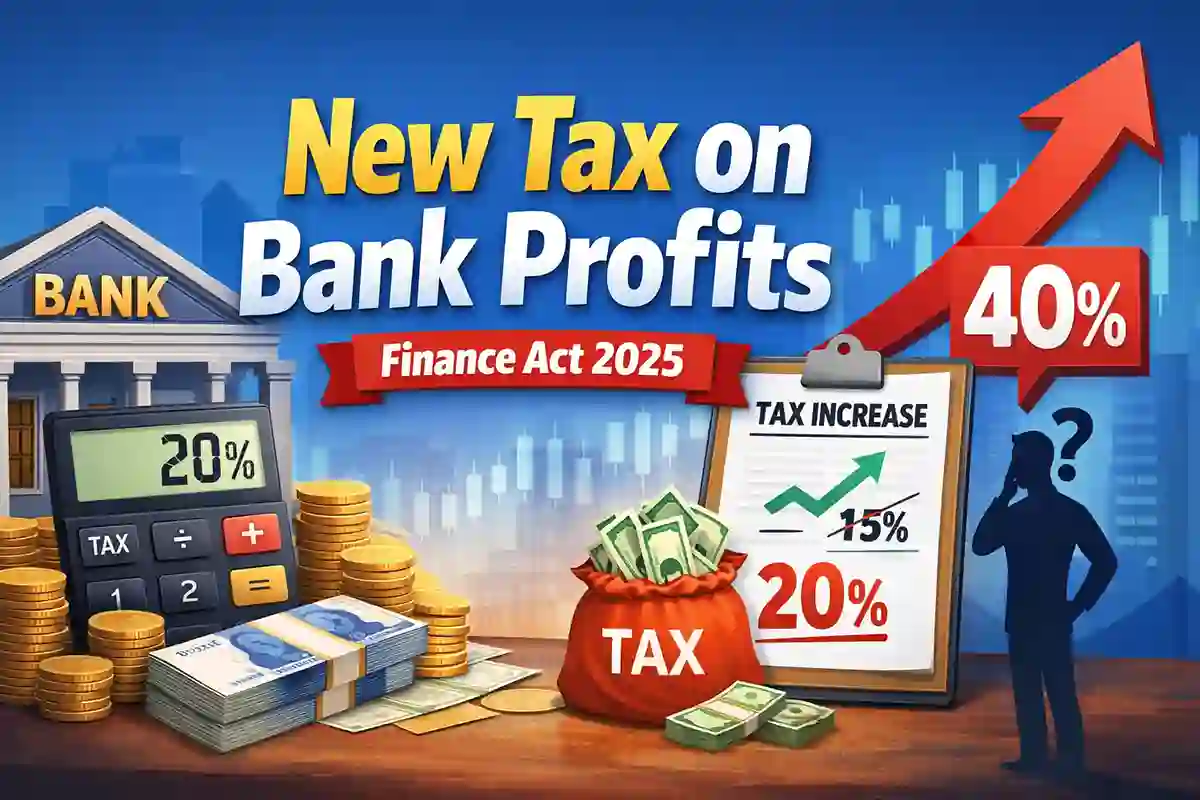

What Has Changed in the Finance Act 2025?

The Finance Act 2025 has increased the tax rate on profit on debt from 15% to 20% for most bank-related deposits.

Key change:

- Tax increased from 15% to 20%

- Applies to bank deposits, financial institutions, and government securities

- Effective from Tax Year 2026 onward

New Tax Rates at a Glance

| Category | Old Tax Rate | New Tax Rate |

|---|---|---|

| Bank savings & deposits | 15% | 20% |

| Financial institutions | 15% | 20% |

| Government securities (general) | 15% | 20% |

| National Saving Schemes | No change | Same as before |

| Post Office Savings | No change | Same as before |

What About National Saving Schemes?

Good news here.

The Finance Act 2025 does NOT change the tax rate on:

- National Saving Schemes (Defense Saving Certificates, Behbood, Pensioner Accounts, etc.)

- Post Office Savings Accounts

These remain taxed under the old structure, which is generally lower or slab-based, especially for senior citizens.

Special Case: Government Securities & Individuals

Another important clarification:

- Profit earned by individuals from government securities is excluded from this increase

- Other investors (companies, institutions) will pay 20% tax

This distinction is important for investors using PIBs or T-Bills directly.

Big Change for Non-Filers (Very Important)

Earlier:

- Non-filers paid a fixed 35% tax on profit on debt

Now:

- That entry has been removed

- From Tax Year 2026 onward, non-filers will pay 100% higher tax

What does “100% higher” mean?

It means:

- If filer tax = 20%

- Non-filer tax = 40%

This is a huge penalty and makes staying a non-filer extremely expensive.

Read more: How to File Tax Return for Salary Person in 2026 in Pakistan

Filer vs Non-Filer Bank Profit Tax Comparison

| Status | Tax Rate on Bank Profit |

|---|---|

| Filer | 20% |

| Non-Filer | 40% |

Conclusion

The Finance Act 2025 clearly shows the government’s intent to increase revenue and encourage tax compliance. While the jump from 15% to 20% may look small, over time it significantly reduces savings. For non-filers, the change is severe and financially damaging.

If you earn profit on bank deposits, being a filer is no longer optional; it’s essential. Smart savers will now focus on after-tax returns, not just profit rates.