Historically, digital content creators, influencers, and online publishers in Pakistan operated in a gray area regarding tax declarations. Recognizing the rapid growth of the digital economy, the Federal Board of Revenue (FBR) introduced a structured, specialized legal framework to formally tax income generated from social media platforms.

Below is a detailed guide explaining the legal logic, the “Deemed Revenue” calculation formula, the relevant Statutory Regulatory Orders (SROs), and how this affects resident and non-resident digital creators.

1. The Legal Framework: Section 99C and SROs

The taxation of digital content creators falls under Section 99C of the Income Tax Ordinance, 2001. To operationalize this section, the FBR issued specific regulations in early 2026:

- S.R.O. 545(I)/2026: Establishes the “Special Procedure for Taxation of Persons Earning Income from Remunerative Social Media Content” for non-residents whose content targets or interacts with users in Pakistan.

- S.R.O. 546(I)/2026: Outlines the parallel special procedure governing resident Pakistani content creators.

Who is Covered?

The tax rules apply to any individual who meets the threshold of “Systemic and Continuous Soliciting of Business Activities or Engaging in Interaction through Digital Means”. The FBR defines this threshold as:

- Having more than 50,000 subscribers or followers during a tax year, OR

- Having more than 12,250 subscribers or followers in a single quarter.

- The regulations also cover accounts with fewer followers but exceptionally high engagement and view counts.

2. The Logic Behind “Deemed Revenue”

Many content creators either receive sponsorship payments through informal channels, receive payments in-kind (free products, travel, merchandise), or fail to declare their actual earnings from platform ad revenue (like YouTube AdSense).

To counter under-reporting, the FBR uses the concept of Deemed Revenue. Instead of relying solely on the bank receipts submitted by the taxpayer, the FBR uses public engagement metrics total posts and average views to calculate what a creator should have reasonably earned.

The Core Formula

The FBR calculates Deemed Revenue using the following formula:

What is RPM?

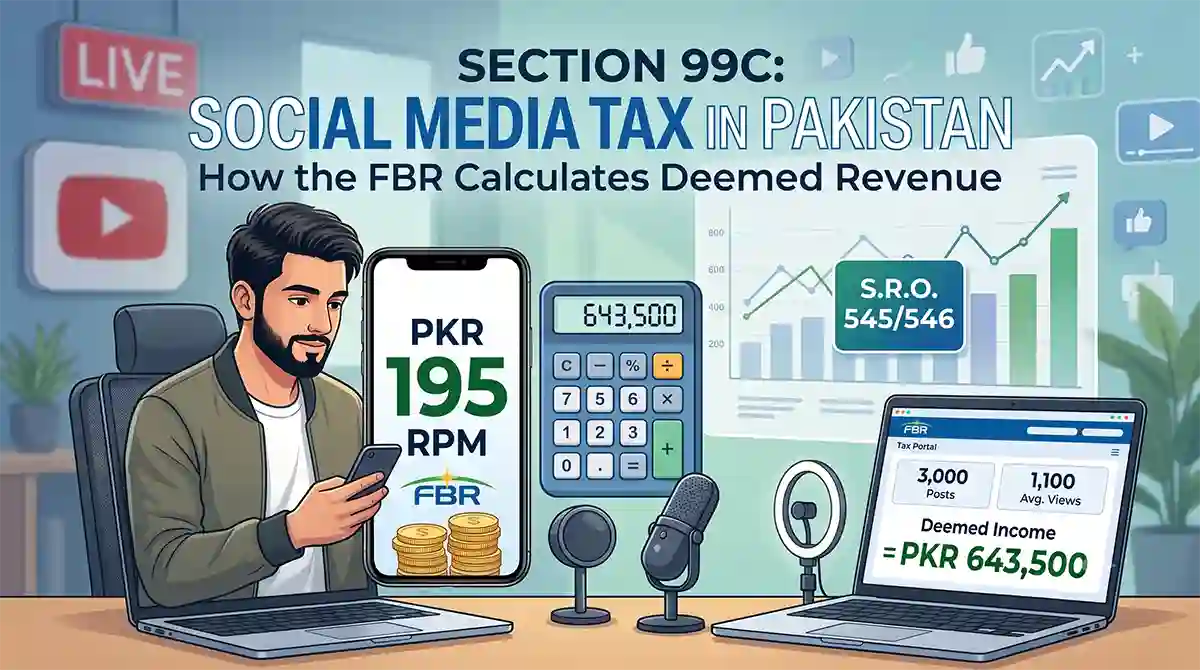

Revenue Per Mille (RPM) represents the estimated earnings a creator receives per 1,000 views. Under the current special procedure, the FBR has locked this benchmark rate at exactly PKR 195 per 1,000 views. This serves as the standardized statutory rate for digital views unless updated by the authority in subsequent tax years.

3. Breaking Down Your Calculation

Using the metrics provided in your tax portal, we can see exactly how the FBR’s system calculated your figures:

- Total Posts (Code 3601): 3,000

- Average Views per Content (Code 3602): 1,100

- Actual Cash Received (Code 3604): PKR 5000

Step 1: Calculate Total Views

Step 2: Apply the FBR RPM Rate

4. The “Higher Of” Rule & Allowed Expenses

The tax portal automatically evaluates both your Deemed Revenue and your Actual Remuneration Received (Cash/Kind). According to S.R.O. 545/546 rules, the FBR treats the higher of the two values as your “Total Revenue” (Code 3605):

Because your calculated Deemed Revenue PKR 643,500 is higher than your actual declared cash receipt PKR 500, the system defaults to PKR 643,500.

Capped Expenses

The law allows you to deduct business expenses (internet, camera equipment, editing software, electricity) up to a maximum cap of 30% of your total revenue.

- In your screenshot, the system calculated Total Expenses (Code 3606) as PKR 500.

- Subtracting your expenses from your Total Revenue gives you the final taxable Income from Social Media Content u/s 99C (Code 3607):

5. Summary of Compliance Requirements

If you qualify under Section 99C, the FBR mandates the following:

- Quarterly Advance Tax: Creators are required to estimate and pay their advance income tax liabilities on a quarterly basis.

- Special Tax Return: Social media income must be declared separately using the designated “Income from Social Media Content” wizard inside your annual tax return portal.

- Audit Risk: Because the FBR keeps track of your public page counts and follower thresholds, under-reporting or omitting this section entirely can trigger automated system audits and subsequent tax recovery proceedings.

For a detailed look at how the FBR is actively implementing these rules on social media influencers and YouTubers, check out this SRO 545/546 and the FBR’s crackdown on digital creators.

Also read:

- Freelancer Tax Calculator 2026-27

- The 1% Fixed Tax Asaan Scheme: Bringing Small Traders into the Tax Net

- Rules for Sending Foreign Remittances in Pakistan (2026 Guide)