The government has introduced an important change in pension taxation through the Finance Act 2025. This amendment modifies how pension income is treated under the Income Tax Ordinance, 2001.

For many years, pension received from a former employer was mostly exempt from income tax. However, the new law removes certain exemptions and introduces taxation on high pension income under specific conditions.

Let’s understand what was happening before, what has changed now, and who will be affected.

What was the position before the Finance Act 2025?

Before this amendment, pensions received from a former employer were generally exempt from tax. The exemption was available under specific clauses of the Second Schedule of the Ordinance.

In simple words, if a person retired and started receiving a pension from their previous employer, that pension was not taxable in most cases. This provided financial relief to retired individuals, especially senior citizens who depended on a pension as their primary source of income.

Only certain private pensions or voluntary pension scheme payments were taxed under Section 39 (Income from Other Sources). But a regular employer-paid pension was largely protected from taxation.

What Has Changed Now?

Through the Finance Act 2025, the government has removed the exemption clauses that previously made employer-paid pension tax-free.

Now, pension received from a former employer is taxable under Section 12(2)(f), but only in certain situations. This means the pension is no longer automatically exempt.

However, the law does not tax everyone. It specifically targets high-income pensioners below a certain age.

Learn more: Salary + Pensioner Tax Return Master Course

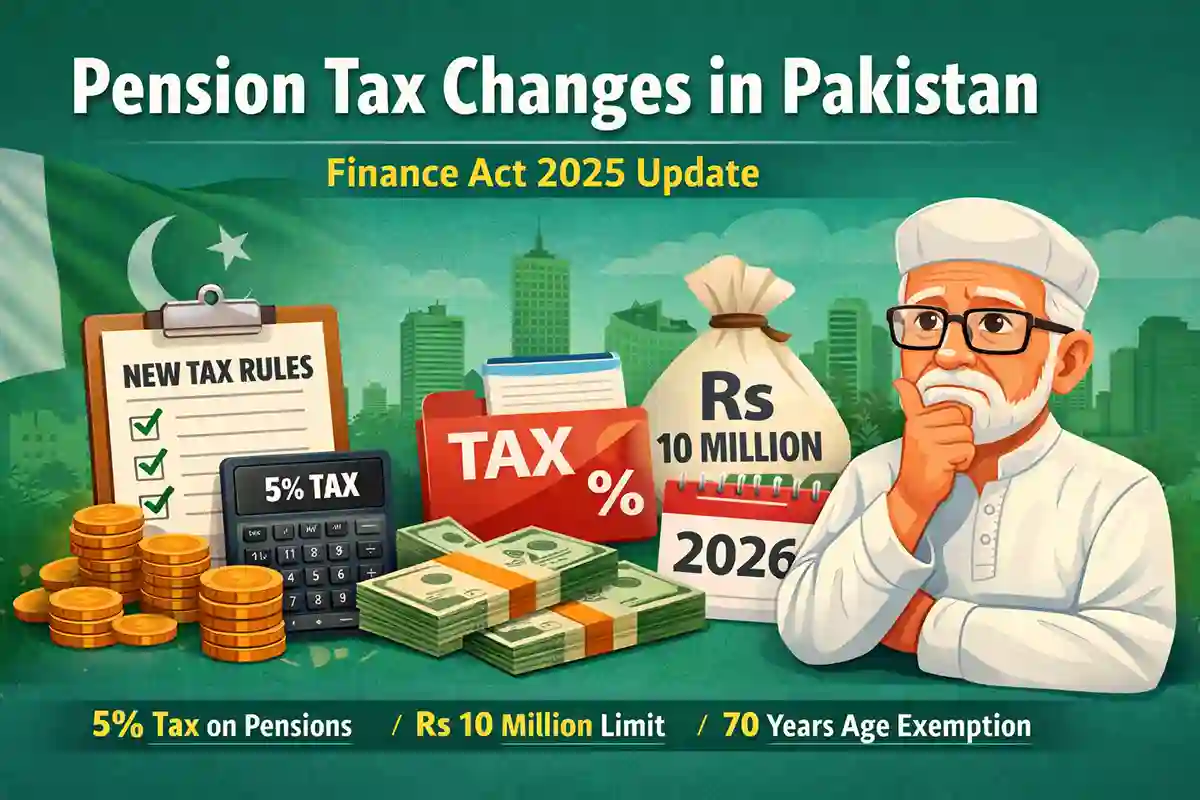

When Will Pension Be Taxed at 5%?

Under the new rule, pension received from a former employer will be taxed at a flat rate of 5%, treated as final tax, if:

- The annual pension exceeds Rs. 10 million (1 crore), and

- The recipient is below 70 years of age.

The term “final tax” means this 5% tax will be the complete and final liability on that pension income. The pensioner will not need to include it again for further tax calculation.

This change mainly affects high-income retirees such as senior executives or individuals receiving large corporate pension packages.

Who Will Not Pay Tax on Pension?

The law clearly protects two categories of pensioners.

First, any person who is 70 years or older will not pay pension tax, regardless of the amount.

Second, if the annual pension is less than Rs. 10 million, it will not be taxed under this new rule. This means small and middle-income pensioners remain unaffected.

What If a Retired Person Continues Working?

An important situation arises where a person retires, starts receiving a pension, but continues to work for the same employer or its associated company.

In such cases, the pension will not be taxed at 5% final tax. Instead, it will be taxed at normal income tax slab rates, just like a salary.

The employer will deduct tax under Section 149 of the Ordinance. If applicable, a 9% surcharge under Section 4AB will also be collected.

So, continuing employment changes the tax treatment significantly.

Read more: How to File a Tax Return for a Salary Person in 2026 in Pakistan

What About Private Pension and Voluntary Pension Schemes?

Pension received from a Pension Fund Manager under the Voluntary Pension Scheme Rules 2005 will continue to be taxed under Section 39 (Income from Other Sources).

This means the Finance Act 2025 has mainly changed the taxation of employer-paid pensions, not private pension funds.

Are Lump Sum Retirement Benefits Still Exempt?

Yes. The law has not removed exemptions for certain retirement benefits.

Commutation of pension (lump sum withdrawal), gratuity, and fifty percent of the balance in a pension account under specific conditions will continue to remain exempt under relevant clauses of the Second Schedule.

So while recurring high pensions may now be taxed, lump sum retirement benefits remain protected.

Practical Examples for Better Understanding

If a 65-year-old retired executive receives Rs. 12 million per year as a pension, he will pay 5% tax on the full amount because it exceeds Rs. 10 million and he is below 70.

If a 72-year-old individual receives Rs. 15 million annually, no tax will apply because he is above 70 years of age.

If a 60-year-old retiree receives Rs. 8 million annually, no tax will apply because the amount is below Rs. 10 million.

If a 62-year-old retiree continues working for the same employer while receiving a pension, the pension will be taxed at normal slab rates, not 5%.

Why Has the Government Introduced This Change?

Although the law does not officially state the reason, the likely objective is to broaden the tax base and increase revenue from high-income individuals.

This change does not target ordinary pensioners. It mainly affects those receiving very large pensions before the age of 70.

Conclusion

Before the Finance Act 2025, pensions from a former employer were largely tax-free. After the amendment, high pension income above Rs. 10 million per year is taxable at 5% if the recipient is below 70 years old.

Small pensioners and senior citizens above 70 remain protected. Lump sum retirement benefits also continue to enjoy exemption.

This amendment represents a shift toward taxing high-income retirees while maintaining relief for ordinary pensioners.

FAQs

These are the most asked questions about the new pension tax rules:

Sir, you have made it so simple and clean. I always appreciate your efforts, and this time it is truly amazing.